IRS Form W-8BEN 2021-2024

Show details

Hide details

Ls. Do not send to the IRS* Department of the Treasury Internal Revenue Service Do NOT use this form if You are NOT an individual Instead use Form. W-8ECI You are a U*S* citizen or other U*S* person including a resident alien individual You are a person acting as an intermediary. W-9 8233 or W-4. W-8IMY Note If you are resident in a FATCA partner jurisdiction i*e* a Model 1 IGA jurisdiction with reciprocity certain tax account information may be provided to your jurisdiction of residence ...

4.5 satisfied · 46 votes

form-w-8ben.com is not affiliated with IRS

Filling out Form W-8BEN online

Upload your PDF form

Fill out the form and add your eSignature

Save, send, or download your PDF

A complete guide on how to Form W-8BEN

Every citizen must declare their finances in a timely manner during tax period, providing information the IRS requires as accurately as possible. If you need to Form W-8BEN, our secure and user-friendly service is here to help.

Follow the instructions below to Form W-8BEN promptly and accurately:

- 01Upload our up-to-date form to the online editor - drag and drop it to the upload pane or use other methods available on our website.

- 02Check out the IRSs official guidelines (if available) for your form fill-out and precisely provide all information required in their appropriate fields.

- 03Fill out your document utilizing the Text tool and our editors navigation to be certain youve filled in all the blanks.

- 04Mark the boxes in dropdowns using the Check, Cross, or Circle tools from the toolbar above.

- 05Make use of the Highlight option to accentuate particular details and Erase if something is not relevant anymore.

- 06Click the page arrangements key on the left to rotate or delete unnecessary file sheets.

- 07Check your forms content with the appropriate personal and financial paperwork to ensure youve provided all information correctly.

- 08Click on the Sign tool and create your legally-binding electronic signature by adding its image, drawing it, or typing your full name, then place the current date in its field, and click Done.

- 09Click Submit to IRS to e-file your report from our editor or select Mail by USPS to request postal document delivery.

Select the best way to Form W-8BEN and report on your taxes online. Try it now!

G2 leader among PDF editors

30M+

PDF forms available in the online library

4M

PDFs edited per month

53%

of documents created from templates

36K

tax forms sent over a single tax season

Read what our users are saying

Learn why millions of people choose our service for editing their personal and business documents.

What Is Form W 8ben?

Today, so many people from different corners of the planet work for the companies registered in the United States. They are not the citizens and do not have the status of the residents. In this case, they need to do something to avoid paying taxes to both the United States and their country of citizenship.

Form W-8BEN is specially designed to solve this problem and simplify the life of a common taxpayer. It is also known as the Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting (Individuals). Different countries have different double income taxation agreements with the United States.

On our site, you will not only find the information how to complete it, but also have a chance to do that electronically, avoiding printers, pens, and, accordingly, uncorrectable errors. Try all editing tools to simplify your life, save time and do everything right. Download and fill out this form for a few minutes.

What is W-8BEN Form Used for?Using Form W-8BEN, you confirm your status of a nonresident of the United States. You must file this form once every two-three years, otherwise you will be required to pay 30% tax. The form must be provided to your income payer, but not to the IRS (Internal Revenue Service).

The form is used to prove that you are not the United States resident and that the money you have received is your income earned on the territory of this country. It must contain a signature of the beneficial owner of that income or the authorized representative. After you submit this form, it will be valid for three calendar years from the date of its signing.

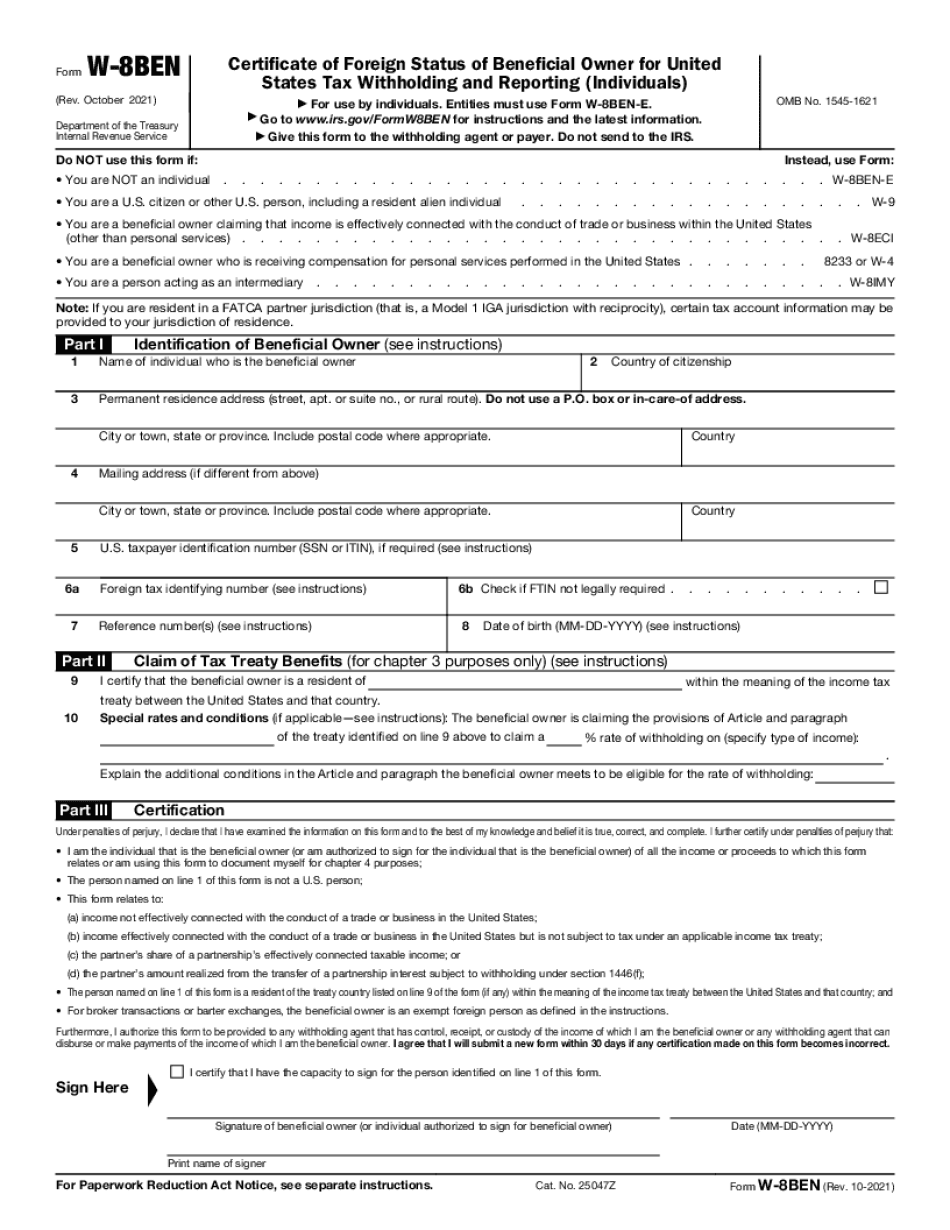

How to Fill out W-8BENNever use Form W-8BEN if you are not an individual. The United States citizens and residents, or intermediaries do not file this. There are generally three parts. In the first part, you must pryour personal information:

- 01name of individual who is the beneficial owner;

- 02country of citizenship;

- 03permanent residence address;

- 04mailing address;

- 05U.S. taxpayer identification number;

- 06reference number;

- 07date of birth.

The second part is devoted to the claim of the tax treaty benefits, where you indicate special rates and conditions. The last part is a certification where you confirm that you understand the possible results of online W-8BEN submission and Pryor agreement. The last step is the signature.

Remember to check the completed form before sending is as you can find lots of mistakes. Edit your PDF document fast and easy using our tools. As a result, you will submit a perfectly filled out form that will definitely be approved.

Online systems assist you to prepare your doc management and boost the productiveness of the workflow. Stick to the fast tutorial with the intention to total Form W-8BEN, prevent glitches and furnish it in a very well timed way:

Questions & answers

Below is a list of the most common customer questions.

If you can’t find an answer to your question, please don’t hesitate to reach out to us.

What is the purpose of Form W-8BEN?

What is the purpose of Form W-8BEN?

(a) General Rule

This Form 8-BEN has been prepared for you by a qualified attorney for use by you personally, a corporate officer, or, with the written permission of the company, a director, in accordance with the requirements of the Internal Revenue Code. The purpose of this Form 8-BEN is to provide the names and addresses of the person(s) to whom any return of tax or other information required under the Code has been (or is going to be) mailed and the address of any office or place of business of the person to which the return or other information relates. This Form 8-BEN need not be furnished to any recipient when the return or other information is mailed to the Secretary. If there is no recipient, the Form 8-BEN needs not be furnished to any person. If your return or other information is transmitted by electronic means to an electronic or other mail address and the electronic address or mailbox for the United States Postal Service is located within New York State, you may enter in your Form 8-BEN the electronic address or mailbox of that electronic address or mailbox. If it is a mailing address other than any location located within New York State, enter in your Form 8-BEN a physical or electronic address (as it appears in your records) for that recipient, along with the name, address and telephone number of the person to whom the return or other information relating to that person shall be addressed and the information described under “How do I mail a Copy of Form 8-BEN?” If it is a physical or electronic address (as it appears in your records) not located within New York State, enter in your Form 8-BEN the location of the physical or electronic address or box so that the recipient may enter in his or her Form 8-BEN a complete mailing address for that person, along with the name, address and telephone number of the person to whom the return or other information relating to that person shall be addressed. The recipient may return the copy of Form 8-BEN that you mailed to him or her using the “addressee” field on Form 843-SS, Form 8443, or Form 8443S. If you mailed the copy of Form 8-BEN using electronic methods, you need not furnish a copy of this Form 8-BEN to anybody for filing purposes.

Who should complete Form W-8BEN?

The Form W-8BEN is for U.S. citizens (individuals) and employers who have employees who live overseas. You should obtain the form from the U.S. Embassy or Consular Section of the country where you want to establish a permanent resident relationship. Please note: Form W-8BEN will not be available at your local U.S. Embassy or Consulate.

If you do not have U.S. employer employees who live abroad, you can use Form W-4 instead. This is a nonimmigrant visa category used to allow businesses and professional groups to bring employees from other countries to work in the U.S. These workers are referred to as “entrepreneurs.” Please refer to Form W-4, Application for Nonimmigrant Worker.

You can also use a commercial travel document if you wish, if you are the business owner whose employees are not eligible for the W-8BEN. You can obtain a commercial travel document by submitting a Commercial Travel Eligibility Document (CITED). This document includes instructions on how to apply to enter Mexico. You can also download a sample form and download it from the Office of Foreign Assets Control's website.

You can find out more about the commercial travel document by using the search box on the Office of Foreign Assets Control's website. We encourage you to download the form and review the information on the form, so you know how to make use of it.

Please be sure you have the correct passport photo. If you do not have a passport, you must apply for a replacement passport. You can find out how to do this online at Mac.gov. If you need a new passport, we may be able to apply for a visa for you.

How do I file Form W-8BEN?

Form W-8BEN can be filed with the U.S. Embassy or Consulate in Mexico or directly with the Department of Homeland Security. Contact the Mexican Embassy in Washington, D.C. at.

Why do I need a Form W-8BEN?

Form W-8BEN is used by companies who have an employee that lives or studies outside the United States. If you have employees in the U.S., but have not established a permanent resident relationship, you must obtain Form W-8BEN and follow the instructions it provides.

When do I need to complete Form W-8BEN?

You must file a Form W-8BEN when you are:

A U.S. citizen or resident alien who receives wages through a regular employee, who is an employer, or on the employee's behalf; or

A nonresident alien who is receiving wages through a regular employee or on the employee's behalf on a permanent or permanent part-time basis.

For more information for residents of the United States and certain other nonresident alien employees, see Publication 517, U.S. Tax Guide for Aliens.

Can I create my own Form W-8BEN?

Yes. There are a number of ways an employer can do so. The first is to take the Form W-8BEN and submit it for each position that it describes. The employer will do the following:

Give written evidence to demonstrate that the employee is actually an employee of the employer.

Submit the form to the employee. To help the employee submit the form, the employer also will provide the employee with a written “notice” detailing what the forms include and giving the employee the chance to review the form.

Provide the employee with a written “notice” that explains how to fill out the form (this is different from the one that the employer will provide).

Mail the Form W-8BEN to the employee to be filled out.

The employer should then file a Schedule H with the Department of Labor to show the number of W-8BEN forms that were submitted and what work the employee has done. The employer can fill out this Schedule H as needed. As part of the Form 990, an employer must include details that identify its W-8BEN activity for the fiscal year and at least one of the following items: The Form W-8BEN was submitted.

The employer paid more than 600 in taxes due for the employee's occupation. Work Hours In general, employers must provide a detailed record of activities in the employee's work day. Employers can use timekeeping records, time sheets, etc. Employers may need to use this information to calculate income and expense claims. Additionally, information gathered at the start of the work day can be important to allow employers to understand how employees will work, whether it will be during regular or off-hours work, and which activities may be part of the job.

For example, if you have employees who have regular and/or weekend and/or evening schedules, and there is an established structure for when they are expected to work, then your schedule can be used as part of the timekeeping record. These schedules are not limited to regular and/or weekend and/or evening schedules, but could also include fixed, flexible or variable hours. In the event that your employees spend time at work in areas that are not part of your structured environment, you can use information gathered through these timekeeping records.

What should I do with Form W-8BEN when it’s complete?

If Form W-8BEN is completed before April 1, 2016, the reporting requirements described in subsection (b) with respect to a corporation are no longer applicable to the corporation and the corporation are also not subject to the reporting requirements under subsections (c) and (d). For information about the reporting requirements for corporations that do not have a Form W-8BEN, see Section 7.03D-1.

For more information regarding an individual's obligation to file Forms W-8BEN, see section 7.03.

7.03-2 -- Reportable payments and payments to other persons (including foreign sources). (a) The reporting entity, regardless of its ownership, shall report any payment that (i) is received as taxable income (other than any deferred payment described in section 7.03-1)-- (A) by the reporting entity on or before October 23 of the taxable year in which the interest expense or the interest income is incurred or is to be incurred, or (B) by a disqualified organization under section 1371, or (ii) is received in the ordinary course of the reporting entity's trade or business and is attributable to an interest expense or an interest income described in paragraph (a)(4)(i)(A) of this section, for all taxable years in which it is received, including any year in which the interest expense or the interest income is incurred or is to be incurred. (4) Interest expense or interest income is-- (A) includible in an amount equal to the tax imposed by section 1 or 2651 with respect to the interest expense, and (B) not includible in paragraph (a)(2)(i) of this section. (5) Determined as of the end of a calendar year. (6) Subsection (a), section 1201, section 1371(a)(5), paragraph or (2) of section 1373(a), or section 1373(a)(3)(A) does not apply with respect to any payment described in paragraph (a)(5)(i)(A) or (6) of this section. (b) If the interest expense or the interest income is incurred by a corporation, the reporting entity shall file Form 1099-DIV, U.S. Report of Foreign Tax Credit, to the extent provided in section 6041(a)(1)(B) or 6655(a)(1)(B).

How do I get my Form W-8BEN?

If you receive a Form W-8BEN from HM Revenue and Customs or you have made use of a HMRC-approved service, you must use their information to prepare your tax returns.

If you have not received a Form W-8BEN, you can use the services of an accountant. The fee is not included in your account. The tax return will be filed by HMRC before it is submitted to your tax return provider.

To find an accountant in your area, enter your postcode on HMRC.gov.

Are you eligible for a form for individuals?

HMRC also publishes online income tax software that can be used to prepare individual returns for the self-employed, sole traders, partnership members/partners, directors, partners and partners in a partnership, and trustees.

How do I prepare a tax return if your business does not meet the current criteria?

Information for those who prepare Individual Tax Returns is also available from HMRC.

What is a company?

What is a sole trader?

How should I include certain expenses?

Do I need to make an entry for all my deductions on my return?

How do I prepare a business return if I am a charity or trustee?

How do I prepare a partnership return if I am an individual or if my partners are not residents of the UK?

What is a sole trader?

Sole traders are individuals who buy or sell solely in their own names, but who also sell on behalf of other entities. A sole trader is not an employee of the seller if they also make, or offer to make, the purchase or sale with the seller's instructions.

If you are a sole trader you will, as a general rule, be required to complete a Form CVS.

If you are an individual or a partner, you can make a voluntary contribution to HMRC to cover all costs associated with conducting a commercial activity in the UK, and you will be required to submit this to HMRC at the time you complete your return.

How should I include certain expenses?

You must report these at Schedule D. You must complete the relevant section of your return each year.

For more information on how to report expenses for each return please see Form CVS and HMRC's general instructions for all returns.

What documents do I need to attach to my Form W-8BEN?

Generally, Form W-8BEN is filed by an employee or agent of the employer. However, you may be able to file and attach an additional form, Form W-8BEN-E, to Form W-8BEN, without an employer. The Form W-8BEN-E is filed by a shareholder, as an agent of a shareholder, or the person's attorney. Examples of this are a shareholder who is the trustee for a trust or corporation's beneficiaries. You may also be able to file and attach a separate Form W-8BEN-E with a Form W-8BEN-E, provided each of the following requirements are met:

The Form W-8BEN is filed from the shareholder or the trustee (or as attorney) of the trust (or as agent of the corporation's beneficiaries).

The Form W-8BEN is filed not later than December 31, 2016.

You filed Form W-8BEN on April 15, 2016, at all times during which you were an officer or director of the corporation unless your name was removed from the proxy statement on August 30, 2017.

The Form W-8BEN or Form W-8BEN-E is submitted and received by the employer or other entity that filed the Form W-8BEN or Form W-8BEN-E.

Important information

Employees (other than those who work for a corporation, partnership, limited liability company, or trust) and employees of the corporation that is the subject of a Form W-8BEN may be subject to additional tax. An employee who claims a loss on a share of stock is subject to an additional tax, known as net worth loss. An employee who claims a loss on the corporation's shares is also subject to an additional tax, known as net worth tax.

What are the different types of Form W-8BEN?

A. The Form 10-K for the fiscal year ending June 30, 2015, is available on the Forms and Publications page under the “Tax” tab.

B. The Form 10-Q for the fiscal year ending December 31, 2013, is available on the Forms and Publications page under the “Tax” tab.

C. The Form 10-Q for the fiscal year ending March 31, 2015, is available on the Forms and Publications page under the “Tax” tab.

D. The Form 10-Q for the fiscal year ending February 28, 2015, is available on the Forms and Publications page under the “Tax” tab.

E. The Form W-2 for the fiscal year ended September 30, 2013, is available on the Forms and Publications page under the “Tax” tab.

F. The Forms W-2A and W-2B for the fiscal years ending March 31, 2013, and 2013 are available on the Forms and Publications page under the “Tax” tab.

G. The Form W-2 for the fiscal year ending March 31, 2013, is available on the Forms and Publications page under the “Tax” tab.

H. The Form 10-K for the fiscal year ending June 30, 2014, is available on the Forms and Publications page under of the “Tax” tab.

I. The Form 10-K for the fiscal year ending February 28, 2014, is available on the Forms and Publications page under of the “Tax” tab.

J. The Form 10-Q for the fiscal year ending December 31, 2014, is available on the Forms and Publications page under the “Tax” tab.

K. The Forms W-2, 10-QA and 10-QE are available on the Forms and Publications page under the “Tax” tab.

L. The Form 10-K for the fiscal year ending June 30, 2015, is available on the Forms and Publications page under of the “Tax” tab.

I-19. I-19F. I-19G. I-19F is a list of all tax tables contained in the publication with a column for each column.

II-18. II-18C. II-18D. II-18E. II-18H. IV-7. IV-7A. IV-7B. IV-7C. IV-7A. IV-7B.

How many people fill out Form W-8BEN each year?

In 2013, there were 2.3 million filings, up from 1.8 million in 1996 and from 200,000 in 1970. As recently as 2000, Form W-8 was issued only once every seven years. In 2014, there were 982,000 filings, an increase from 875,000 in 2013.

What is W-8BEN, and why does IRS issue it?

Form W-8BEN is a self-employment tax form commonly referred to as a W2BEN or W-2BEN. The form is issued to people who have earned income from self-employment and are required to file their own tax returns. The form contains information about the income generated, the source from which the money comes, the business entity the income is earned on and whether the income qualifies for tax deductions. As it relates to wages, income earned while the person is working for another person could qualify for an overtime exclusion if the employee and his or her employer can agree to it.

When the information is completed, the form is sent to the IRS, who then decides whether to file the individual a 1040 tax return, Form W-2, and Form 8962, Wage and Tax Statement. If no deduction is allowed for the income, no refund is ever issued until the individual returns and files Form W-8BEN.

When can you file it?

You do not want to leave it to the IRS to determine if there is any tax deducted. You can start collecting this information now and get it sent to you automatically. The IRS sends out W-8BEN forms in the months of April, July, October and November. They should be available for you to process as soon as they become available.

You will need the following information to complete the W-8BEN:

If the individual earned their income from self-employment: Social security numbers (SSN).

Date of birth (DD/MM/BY);

Social Security number or employer SSN, if the individual is filing as a sole owner. If the individual is filing as a partner or joint owner, both the employer and the individual's SSN are required. If someone else is getting benefits from the individual for the sole purpose of getting the self-employment income tax deduction, the same requirements apply.

Is there a due date for Form W-8BEN?

If you make an election to use Form W-8BEN before the due date, you must file the form. However, if you later use Form W-8BEN after the due date, you must file it within 2 years after the due date of the original Form W-8. You may qualify for a refund in either case.

Return to Top

Are there tax-free years in 2018?

Yes, there are 3 tax-free or reduced-rate years: 2018, 2017, and 2016.

If you were paid in the 2017 or 2016 tax year, and you qualify for a tax holiday, you should file your tax return by April 15, 2018. However, there are some situations and/or situations in which you may need to file your return by December 15, 2017. For more information, see the IRS article.

If you paid in 2017 or 2016, but you were paid in 2017 or 2016 (or made your payment in 2017) and you qualify for a tax holiday, you can file the 2017 or 2016 return by April 15, 2018. However, if you made your payment in 2017 or 2016, and you qualify for a tax holiday, you can file the 2017 return by December 15, 2017.

If you pay in 2017, and you qualified for a tax holiday in 2017, you can file the 2018 return by February 16, 2018.

Return to Top

Are there tax-free months in the 2017 tax year?

Yes. The total month tax-free from the 2017 tax year is 15 consecutive days, from April 17 to October 30, 2017. You can use this 15-day period if you can't prepare and file your return for the 2017 tax year because you are a United States citizen or resident alien, certain other U.S. nationals, or aliens legally present in the United States.

Return to Top

Are there tax-free months in the 2016 tax year?

Yes. The total month tax-free from the 2016 tax year is 10 consecutive days, from the April 17 tax-free days to the last day to file the 2016 tax return for any year. You can use this 10-day period if you can't prepare and file your return for any year because you are a United States citizen or resident alien, certain other U.S. nationals, or aliens legally present in the United States.

If you believe that this page should be taken down, please follow our DMCA take down process here